import matplotlib

if not hasattr(matplotlib.RcParams, "_get"):

matplotlib.RcParams._get = dict.get

Estimation of a single sample vs many samples#

Starting with the estimation of a single sample

We have seen that observations have random errors. This is is evident from our observation Model:

This means that when the same experiment is repeated under the same circumstances, each repetition should produce a different realisation of the observation vector \(Y\)

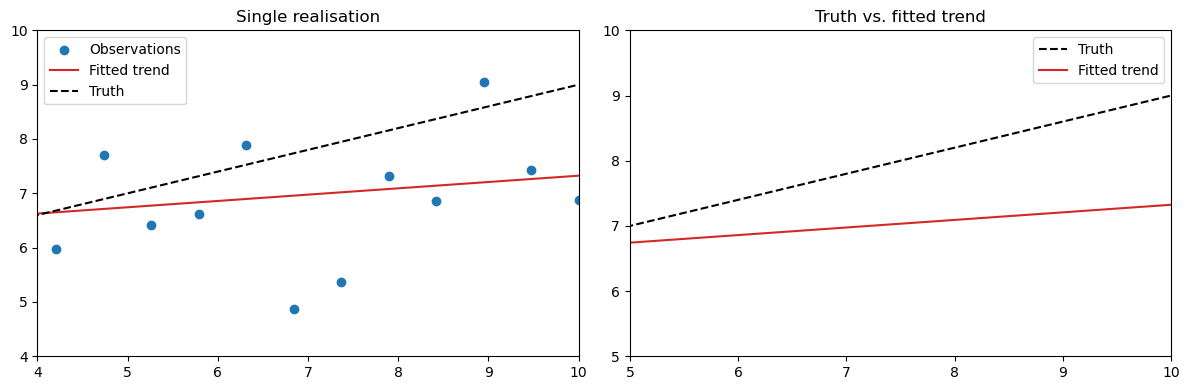

For one such realisation we can use BLUE:

For an individual realisation of \(\hat{X}\) you will find that it deviates from the “true” \(\mathrm{x}\) due to the measurement noise.

Below we set up the model to make an estimation of a single realisation and compare it with the “truth”.

Click –> Live Code on the top right corner of this screen and then wait until all cells are executed.

import numpy as np

import scipy as sc

from scipy.stats import norm

import matplotlib.pyplot as plt

%matplotlib inline

from ipywidgets import Button, VBox, Output

# BLUE function

def blue(A, y, Sigma_Y):

W = np.linalg.inv(Sigma_Y)

x_hat = np.linalg.inv(A.T @ W @ A) @ (A.T @ W @ y)

return x_hat

# Set up observation model

np.random.seed(42)

m = 20

t = np.linspace(0, 10, m)

A = np.column_stack((np.ones(m), t))

# the "true" parameters and "true observations"

x_true = np.array([5.0, 0.4])

sigma = 1.5

Sigma_Y = sigma**2 * np.eye(m)

y_true = A @ x_true

# Generate a single realisation (with noise)

y = A @ x_true + np.random.normal(0, sigma, m)

#estimated parameters

x_hat = blue(A, y, Sigma_Y)

y_hat = A @ x_hat

# Plot the results

# Left: Observations and fit

fig, ax = plt.subplots(1, 2, figsize=(12, 4))

ax[0].scatter(t, y, label='Observations', color='tab:blue')

ax[0].plot(t, y_hat, color='tab:red', label='Fitted trend')

ax[0].plot(t, A @ x_true, 'k--', label='Truth')

ax[0].set_title('Single realisation')

ax[0].legend()

ax[0].set_xlim(0, 10) # Fixed x-axis limits

ax[0].set_ylim(4, 10) # Fixed y-axis limits

# Right: True vs fitted

ax[1].plot(t, A @ x_true, 'k--', label='Truth')

ax[1].plot(t, y_hat, color='tab:red', label='Fitted trend')

ax[1].set_title('Truth vs. fitted trend')

ax[1].legend()

ax[1].set_xlim(0, 10) # Fixed x-axis limits

ax[1].set_ylim(4, 10) # Fixed y-axis limits

plt.tight_layout()

plt.show()

Repeated Realisations and Convergence of the Estimator#

In the previous chapter, you explored the concept of a Monte Carlo simulation and how repeated sampling can be used to approximate the behaviour of random variables.

The model above shows one possible realisation of our noisy observation vector \(Y\). We will now show that if we would repeat the same experiment many times the observations and therefore the fitted model would change. Every repetition gives a new estimate and model:

where each \(\epsilon^{(k)}\) is an independent random sample from

\(\mathcal{N}(0,\,\Sigma_Y)\)

Because the BLUE estimator is unbiased, the expected value equals the true values:

This means that if we take many independent samples and compute the empirical mean

then as the number of repetitions \(N\) increases, the mean will converge to the true mean:

In other words, by averaging over many realisations, the random estimation errors cancel out,

and the mean of all fitted trends converges to the true trend.

Below you can experiment with this principle with the interactive plot.

Each time you click “New realisation”, a new noisy dataset is generated and fitted using BLUE (just like we did in the code above for a single realisation). All realisations are stored and averaged each time you sample again:

The left plot shows the current set of noisy observations and its fitted trend.

The right plot accumulates all fitted trends and shows their running mean (red) together with the truth.

Try clicking the button: New Sample to add a realisations and see what happens to the red mean line and the black dashed “true” line. (click to resample a couple of times, the more the better)

# BLUE function

def blue(A, y, Sigma_Y):

W = np.linalg.inv(Sigma_Y)

x_hat = np.linalg.inv(A.T @ W @ A) @ (A.T @ W @ y)

return x_hat

# Set up observation model

np.random.seed(42)

m = 20

t = np.linspace(0, 10, m)

A = np.column_stack((np.ones(m), t))

# the "true" parameters and "true observations"

x_true = np.array([5.0, 0.4])

sigma = 1.5

Sigma_Y = sigma**2 * np.eye(m)

y_true = A @ x_true

# Generate a single realisation (with noise)

y = A @ x_true + np.random.normal(0, sigma, m)

#estimated parameters

x_hat = blue(A, y, Sigma_Y)

y_hat = A @ x_hat

# Storage for single realisations results

x_estimates = []

y_estimates = []

# Plot function for a single realization

def plot_single_realization(A, t, x_true, sigma, x_estimates):

y = A @ x_true + np.random.normal(0, sigma, len(t))

x_hat = blue(A, y, sigma**2 * np.eye(len(t)))

x_estimates.append(x_hat)

y_hat = A @ x_hat

y_estimates.append(y_hat)

# Compute current mean and covariance of estimates

X_array = np.array(x_estimates)

x_mean = np.mean(X_array, axis=0)

y_mean_fit = A @ x_mean

# --- PLOTS ---

fig, ax = plt.subplots(1, 2, figsize=(14, 6))

# Left: new realization and fitted trend

ax[0].scatter(t, y, label='Observations', color='tab:blue')

ax[0].plot(t, y_hat, color='tab:red', label='Fitted model')

ax[0].plot(t, A @ x_true, 'k--', label='Truth')

ax[0].set_title(f'Realisation {len(x_estimates)}')

ax[0].legend()

ax[0].set_xlim(0, 10) # Fixed x-axis limits

ax[0].set_ylim(4, 10) # Fixed y-axis limits

# Right: mean of all fits so far + 95% conf. region

ax[1].plot(t, A @ x_true, 'k--', lw=2, label='True trend')

for i in range(len(y_estimates)):

ax[1].plot(t, y_estimates[i], 'gray', alpha=0.3)

ax[1].plot(t, y_mean_fit, 'r-', lw=2, label='Mean fitted model')

ax[1].set_title(f'Mean model after {len(x_estimates)} realisations')

ax[1].legend()

ax[1].set_xlim(0, 10) # Fixed x-axis limits

ax[1].set_ylim(4, 10) # Fixed y-axis limits

plt.tight_layout()

plt.show()

# Interactive control

out = Output()

def resample(_):

with out:

out.clear_output(wait=True)

plot_single_realization(A, t, x_true, sigma, x_estimates)

# Create button

button = Button(

description="Click: New sample",

button_style='info',

tooltip='Click to generate a new noisy sample and update the mean trend.'

)

button.on_click(resample)

# Display initial realization

with out:

plot_single_realization(A, t, x_true, sigma, x_estimates)

# Display button and output area

display(VBox([button, out]))

You can see the convergence after taking many new samples and if we plot all those individual fitted models we can see grey region being formed, this is a realisation of the confidence region. Lets below take a montecarlo simulation to show what it looks like after many realisations, making \(N\) very large. Feel free to move the slider to increase the samples and see what happens with the confidence region after many \(N\) realisations.

from ipywidgets import interact, IntSlider

# BLUE function

def blue(A, y, Sigma_Y):

W = np.linalg.inv(Sigma_Y)

x_hat = np.linalg.inv(A.T @ W @ A) @ (A.T @ W @ y)

return x_hat

# Set up observation model

np.random.seed(42)

m = 20

t = np.linspace(0, 10, m)

A = np.column_stack((np.ones(m), t))

# The "true" parameters and "true" observations

x_true = np.array([5.0, 0.4])

sigma = 1.5

Sigma_Y = sigma**2 * np.eye(m)

y_true = A @ x_true

# Function to run N realisations and plot result

def monte_carlo_simulation(N=100):

x_estimates = []

y_estimates = []

for _ in range(N):

y = A @ x_true + np.random.normal(0, sigma, len(t))

x_hat = blue(A, y, sigma**2 * np.eye(len(t)))

x_estimates.append(x_hat)

y_estimates.append(A @ x_hat)

# PLOT

plt.figure(figsize=(10, 6)) # Larger figure size for better visibility

# Plot N random individual realizations

for i in range(N):

plt.plot(t, y_estimates[i], color='gray', alpha=0.3)

plt.plot(t, A @ x_true, 'b--', lw=2, label='True trend')

plt.title(f'{N} fitted trends')

plt.legend()

plt.xlim(0, 10)

plt.ylim(4, 11)

plt.tight_layout()

plt.show()

# Interactive slider for N

interact(monte_carlo_simulation, N=IntSlider(value=10, min=1, max=2000, step=10, description='Realisations'));